The Trump tax cuts, sometimes known as the Tax Cuts and Jobs Act (TCJA), that were enacted in late 2017 disproportionately cut taxes for wealthy individuals and large profitable corporations.1 In crafting their bill, the Republican trifecta chose to make the corporate provisions of that bill largely permanent, and they chose to set most of the portions that affect individuals to expire after eight years, at the end of 2025, to keep the scored cost of their bill artificially small.

With large portions of the law set to expire at the end of next year, Congress is debating how much of these tax cuts to extend and whether to offset any of the cost. A full extension of the expiring individual side provisions would add roughly $4 trillion in costs to the approximately $2 trillion in costs that the 2017 law has already incurred.2

Daunted by the prospect of being held responsible for spending trillions more dollars on tax cuts, leading Republican tax legislators such as Sen. Mike Crapo (R-ID) have proposed a solution to the problem: just pretend the tax cuts do not cost anything.3 This would be accomplished by switching from the “current law baseline” congressional Republicans exploited when the tax cuts were initially passed in 2017 to a “current policy baseline” for the extension in 2025. This gimmick would produce a “double no count” wherein Congress never counts trillions of dollars of tax cuts in 2017 or 2025.

A fundamental rule of budgeting is that all costs must be shown at some point. They can all be shown up front when legislation is enacted permanently, or they can be shown along the way—during the original temporary bill and during each subsequent extension. But all costs must at some point be recognized. The double no count allows them to avoid being counted in either bill.

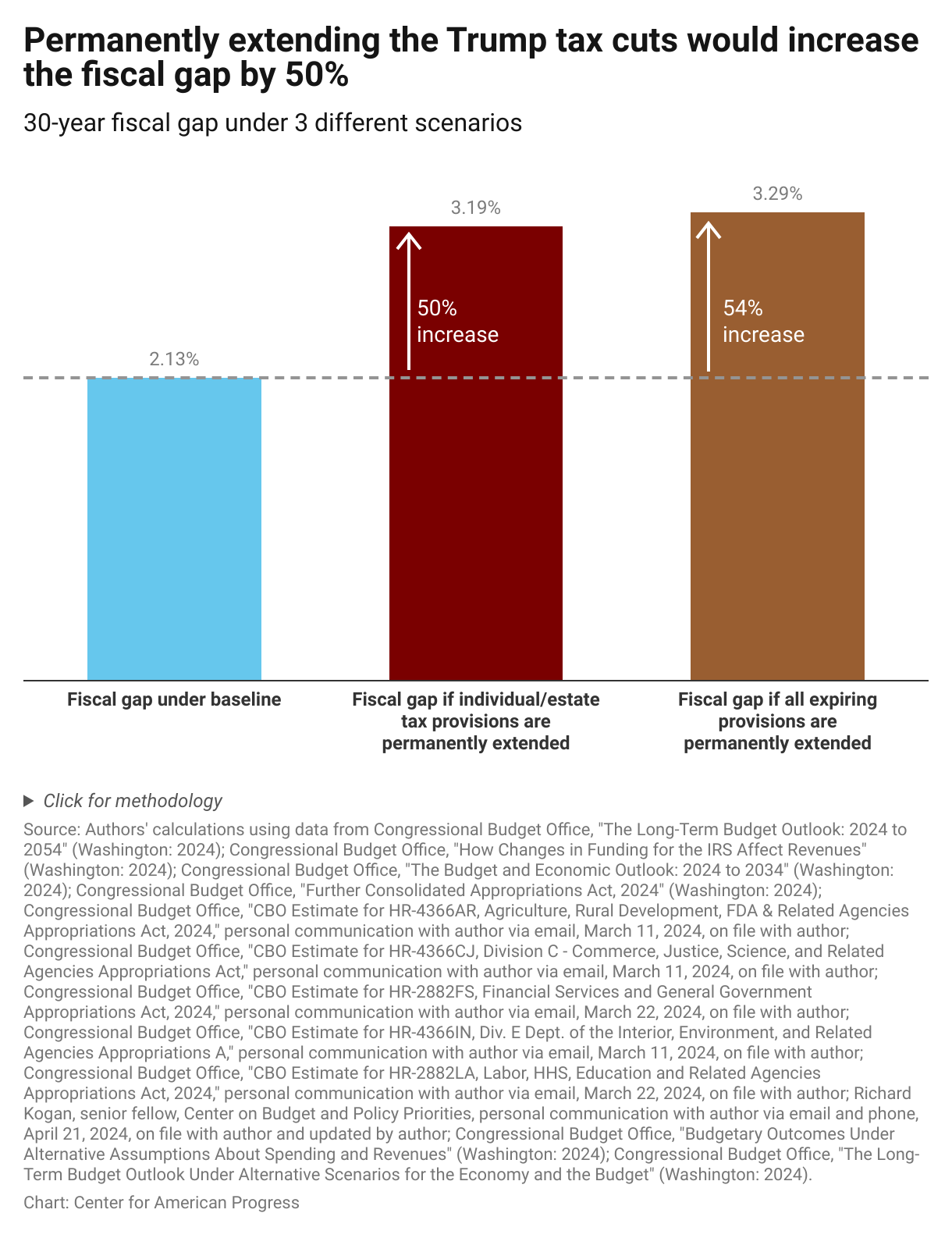

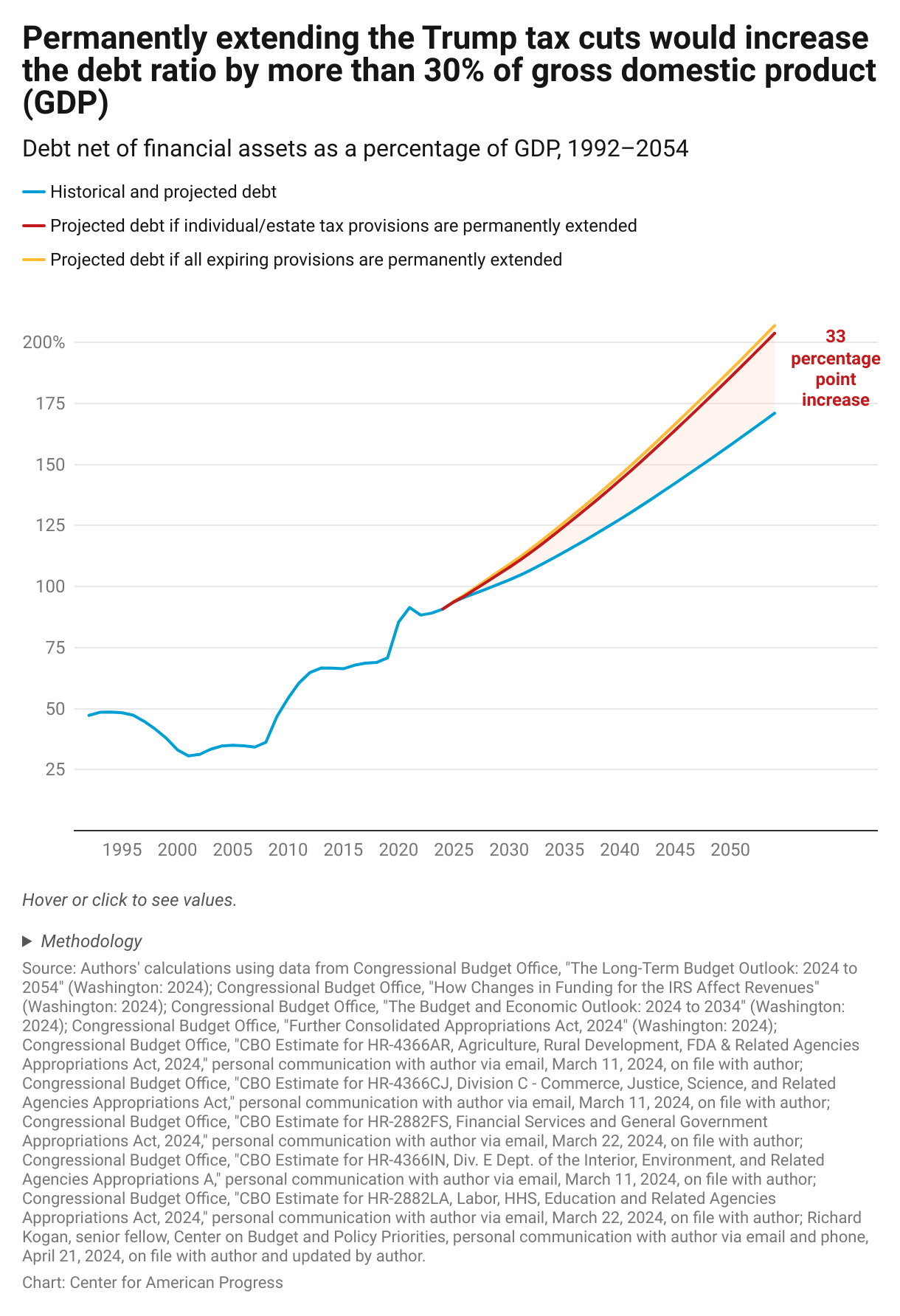

The double-no-count gimmick is not only dishonest, but it deliberately hides the cost of tax cuts and sets up cuts to programs that will hurt American families. Making the Trump tax cuts permanent will increase upward pressure on the federal debt-to-gross domestic product (GDP) ratio by 50 percent and put the federal debt on a path to hit 204 percent of GDP by 2054. These types of deficits and debt trajectories have historically been used to justify cuts to important budget programs on which Americans rely.

The congressional Republicans pushing for a current policy baseline argue that, because Americans have been living under this tax code for a handful of years now, continuing that policy does not change anything and therefore is costless, while allowing these taxes to expire should be viewed as a tax increase.4 But rhetoric cannot change the fact that extending the Trump tax cuts without an offset will result in trillions of dollars in additional costs, on top of the $2 trillion cost of the original Trump tax cuts. That means lower revenues and higher deficits, regardless of which baseline is used.

This report explains how the double-no-count gimmick works and how, contrary to the claims of Sen. Crapo and others, it differs from other programs’ consistent use of a current policy baseline. What Sen. Crapo is asking for is special treatment that no part of the budget has ever received in official budget enforcement.

What is the difference between current law and current policy?

One to three times per year, the Congressional Budget Office (CBO) releases a projection of the budget outlook for the coming 10 years, known as the CBO baseline.5 The CBO baseline makes a series of budgetary and economic estimates, including revenues, various components of spending, deficits, and debt. It also includes GDP growth, the interest rate on government debt, and inflation. This baseline is constructed pursuant to the rules written into budget law in 1990.6 It is sometimes known as the current law baseline. However, some congressional Republicans are trying to use an alternative projection—a current policy baseline—to facilitate extending the expiring portions of the Trump tax cuts.

What is the current law baseline?

The current law baseline that is used in the budget resolution or deeming resolution is known as the scoring baseline, and the CBO and the Joint Committee on Taxation (JCT) are tasked with estimating the budgetary effects of legislation relative to it.

Under the current law baseline, for the most part, CBO projections assume that bill provisions that lawmakers set to expire actually do expire and that permanent provisions stay permanent. Annual appropriations funding is assumed to be the same level it was in the year before, adjusted for inflation, and funding for entitlement authority is assumed to be adequate to make all payments required by those laws.7 This means that the cost of extending an expiring provision is the same as creating it from scratch because legislation is scored relative to the baseline and because the baseline assumes provisions lawmakers chose to let expire do in fact expire.

What is a current policy baseline?

Most of the individual tax cut provisions of the Trump tax cuts are set to expire at the end of 2025.8 This means that the current law baseline assumes their expiration, and any bill to extend them would be scored as costing trillions of dollars.

But the alternative current policy baseline that some Republicans have proposed—either for rhetorical purposes or for official CBO/JCT scoring and budget enforcement—would change the assumption that the Trump tax cuts that are set to expire under the law to instead assume that they will actually continue. Doing so would make it appear as if a bill extending them is free, despite the fact that an extension of the individual and estate tax cuts would cost taxpayers roughly $3.9 trillion over 10 years that has never been counted, increasing upward pressure on the debt-to-GDP ratio by 50 percent.9

Republican tax legislators are proposing to increase deficits using a fast-track Senate procedure

It is first worth examining why a baseline matters for tax legislation next year. Congress has the power to pass permanent deficit-increasing tax legislation through the normal legislative process, but doing so requires 60 votes to pass the Senate, and Republican tax legislators appear intent on passing a party-line tax bill next year, just as they did in 2017.

The budget reconciliation process makes budgetary legislation easier to pass, requiring only a simple majority in the Senate—an avenue not available to nonbudgetary legislation—but it has to conform to certain rules.10 One of those rules is that titles of reconciliation bills may not increase the deficit in any year beyond the 10-year budget window with only a simple majority of votes.11 Another rule is that the legislation must meet its 10-year budgetary target that Congress decides when it passes a budget resolution, which is the first step toward passing a reconciliation bill.

This is where the choice of the baseline becomes important. The individual portions of the 2017 tax cuts are set to expire after 2025. Making them permanent would have a roughly $4 trillion 10-year cost and create deficits outside of the 10-year window, using the official current law baseline. But using a current policy baseline would treat their extension as having a 10-year cost of zero and would not add to long-term deficits. This is leading some Republican legislators such as Sen. Crapo to try to use the current policy baseline, to help with both the politics and the procedure.

Switching to current policy would be a budget gimmick that produces a double no count

The point of producing budget scores is to give lawmakers an accurate sense of how proposed legislation will affect the budget. In order to do that, the scores have to have a consistent set of basic rules and assumptions, and the full cost of a policy must always be reflected somewhere. Congress is always allowed to increase deficits, but the point is for them to have good information. Switching baselines does not change the true cost of legislation—it obscures it.

The costs of provisions in legislation can be accounted for in one of two ways. The costs of permanent provisions are counted only once in the law that creates them. The costs of temporary provisions are counted when they are initially passed until their expiration, and then each time they are extended. But as a fundamental rule of budget scoring, all costs are counted at some point.

However, if something was scored as temporary under a current law baseline on the way in, then switching to a current policy baseline to make it permanent after the fact is a gimmick that allows portions of the cost to never be counted, even though the costs are real.

For the Trump tax cuts, switching to a current policy baseline would allow roughly $4 trillion in additional deficits without those costs ever being counted. This produces a “double no count.” These costs were deliberately excluded when the Trump tax cuts passed because the lawmakers wrote them to expire after eight years, and they would also not be counted now because the lawmakers are using a baseline that assumes they are permanent.

This is particularly egregious because the Republican tax legislators deliberately turned off the Trump tax cuts artificially early when they enacted their bill in 2017. Because Republican legislators did not want to pay for their tax cuts, they would have needed to turn off their tax cuts after 10 years to avoid long-term deficits—both a rule of budget reconciliation and a permanent rule created in the fiscal year 2016 budget resolution. But the Trump tax cuts expired after eight years, not 10, because legislators could not fit all of their desired tax cuts into the binding $1.5 trillion limit they imposed on themselves in their budget resolution and did not want to make the cuts smaller. This produced more than $300 billion in artificially lower costs within the 10-year window, while avoiding showing any costs beyond the 10-year window.12

But by switching to a current policy baseline, the costs of an extension will never be counted. Republican tax legislators wanted the scoring benefits of being temporary when it was time for enactment in 2017—even though they had no intention of the taxes being temporary—and now they want the scoring benefits of being assumed to be permanent when it comes time for extension in 2025.

Switching from a current law baseline to a current policy baseline is a red flag in budget enforcement

Critically, switching between a current law baseline treatment and a current policy baseline would mean that the scoring for the initial law would be inconsistent with its extension. Had the 2017 tax law been scored with a current policy treatment, its scoring benefits would not have been allowed.

The CBO assumes that some temporary budget programs continue in the baseline, but they do so consistently. Temporary programs that are assumed to continue in the baseline are scored recognizing all costs over the course of the 10-year window, even if the extension is temporary. For example, Congress typically reauthorizes the Supplemental Nutrition Assistance Program (SNAP) for five years at a time, but the CBO uses a current policy treatment for evaluating its costs. (see text box)

How SNAP is scored using a consistent current policy baseline

Despite only being authorized for five years at a time, the CBO baseline assumes that the budgetary costs of SNAP continue over the full 10-year scoring window.13 In effect, the budget baseline and scoring rules treat the existing SNAP program as being permanent. Its reauthorization at the baseline levels is therefore scored as not increasing costs because those costs are already assumed to happen.

But this means that increases above baseline are also assumed to continue—to be permanent—even beyond the period of extension. If a SNAP reauthorization increased spending by $10 billion per year for its five-year reauthorization, the CBO score would nonetheless show $100 billion in costs: $50 billion for the five years that are being reauthorized, and then $50 billion for the years the baseline assumes it will be reauthorized again at this higher level.

The only way to avoid that is to turn off the cost inside the reauthorization. If instead Congress chose to increase SNAP by $10 billion per year for the first four years of the reauthorization and then set it back to the baseline level, not only would there be no cost in year five, but there would be no extra cost in years six through 10. But then when Congress wanted to increase SNAP benefits four years from now (instead of five) to prevent the $10 billion annual increase from expiring in year five, that prior $10-billion-per-year increase would not be assumed in the baseline. That $10 billion increase would not receive current policy treatment. And as a result, the bill would once again have to be scored with increasing the cost of SNAP by $10 billion per year, and it would be scored not just for the fifth year but for each subsequent year.

If the Trump tax cuts had received the same consistent current policy baseline treatment as all temporary provisions that the CBO assumes will continue, such as SNAP, the CBO would have said the bill costs $1.8 trillion.14 This would have run afoul of the Senate’s rules of reconciliation both by exceeding the binding $1.5 trillion limit self-imposed by the budget resolution and by adding to deficits beyond the 10-year window. The 2017 tax bill would not have been able to turn the costs off after eight years to achieve a lower score if it had been scored with a current policy baseline. Otherwise, the Trump tax cuts would no longer be able to be assumed to continue in the baseline, as in the four-year SNAP example in the text box above.

The Republicans tax legislators calling for a current policy baseline in 2025 want their tax cuts to get special treatment to have it both ways: They want the benefits of being scored on a temporary basis for its enactment in 2017, and then they want the benefits of being scored on a current policy baseline when it comes time for extension. They relied on current law scoring to make their bill look artificially cheap in 2017, and now they want to rely on current policy scoring to make their bill look artificially cheap in 2025.

That is a gimmick. That is a double-no-count, and no program in the entire budget is officially scored this way.

Imagine, for example, if congressional Democrats had said that permanently extending the American Rescue Plan Act’s (ARPA) one-year child tax credit expansion were free, on the grounds that it was just extending current policy. And even more absurdly, imagine if congressional Democrats in 2022 had asserted that the $1.9 trillion temporary ARPA that they passed in budget reconciliation in March 2021 were now “current policy” and Congress could then claim $19 trillion in savings by letting it expire on schedule. They then could have used those savings to “pay for” the Build Back Better agenda with no tax increases, while claiming more than $10 trillion dollars in deficit reduction by letting the ARPA programs expire as scheduled. Either of these scenarios would have been a gimmick.

Switching after the fact to a current policy baseline is not a principled budgetary perspective—it is a maneuver to solve a political problem by making the tax cuts appear free when they are not. Extending the Trump tax cuts would be very expensive, and it looks bad for members of Congress with debt counters at the top of their official websites to vote for legislation that adds trillions of dollars to the debt.

A small percentage of both temporary spending and temporary revenues provisions are assumed to continue in the CBO baseline

Many Republicans, including the leading Senate Republican tax legislator, incorrectly say that the CBO baseline assumes temporary spending changes continue but temporary revenues changes do not, so they are just seeking baseline parity between spending and revenues.15

This is not true. The CBO baseline assumes some amount of both temporary spending and revenues continues, but only a small portion of each.

Temporary spending programs that cost at least $50 million and were established on or before 1997 are assumed to continue in the baseline in the same manner as the program operated immediately before its expiration. All spending programs of at least $50 million that have been created since then are only assumed to continue if the budget committees instruct the CBO to have them continue in the baseline.16 Only negligible amounts of spending have been added to this list since 1997. Temporary mandatory programs that are assumed to continue—such as SNAP—make up slightly less than 3 percent of total mandatory spending.17

Excise taxes dedicated to a trust fund, if expiring, are assumed to be extended at current rates.18 These taxes make up around 1 percent of total revenue.19 And as with the program spending that is assumed to continue, this treatment does not allow for new costs to achieve a double no count.

Regardless of whether a program is assumed to continue in the baseline or not, official scores from the CBO recognize all costs at some point. Switching to a current policy baseline for official enforcement of the Trump tax cuts would be an anomaly, giving them special treatment that no other legislation receives.

The double no count is bad for deficits, adequate revenues, and adequate spending

Using a current policy baseline to make expensive tax cuts appear free is the same maneuver that was used to pass, and later make permanent, the vast majority of the Bush tax cuts between 2001 and 2013.20 The original Bush tax cuts were also made temporary to comply with reconciliation rules against adding to deficits beyond the 10-year window, and thus avoided trillions of dollars of costs being enforced. However, policymakers of both parties began discussing their extension in current policy terms rhetorically, and so extending them was considered free.

This ended in January 2013, when roughly 85 percent of the Bush tax cuts were made permanent in the American Taxpayer Relief Act of 2012.21 But instead of accurately describing these tax cuts as costing $3.9 trillion (or $6.8 trillion in today’s terms), the Obama administration and a bipartisan Congress wrongly sold the bill as a tax increase of $618 billion on the richest Americans, incorrectly claiming it reduced the deficit when it was, in fact, the reason the United States has a fiscal gap.22 Had the Bush tax cuts never been extended, revenues would be on track to keep pace with primary spending indefinitely, leaving the long-term debt-to-GDP ratio stable.23

Adopting the same process with respect to the Trump tax cuts will deliver a similar result: Permanently extending the individual side and estate tax portions of the Trump tax cuts would increase upward pressure on the debt-to-GDP ratio by 50 percent and leave debt above 200 percent of GDP by 2054.24

Adopting a current policy baseline to extend the Trump tax cuts in 2025 will make it easier not only to pass a simple extension, but also to pass even more tax cuts. For instance, under a current law baseline, extending the individual and estate tax portions of the Trump tax cuts and eliminating the taxation of tipped income and overtime pay would cost $4.9 trillion through 2035.25 But under a current policy baseline, that same bill would only have a headline cost of $900 billion, making its passage easier.26

Moreover, this sets the stage for even more fiscal recklessness down the road: If bills can be consistently scored for only eight years and then have their extension appear free, Congress will habitually adopt the same approach to hide even larger costs over periods of time. There would be no reason for Congress to not make its next tax cut bill a $4 trillion tax cut over four years instead of 10 years.

Deficits from tax cuts have historically been used to justify cuts to important budget programs. The high deficits the Reagan tax cuts produced were used to justify program cuts in the Reagan, Bush, and Clinton administrations.27 The high deficits produced by the Bush tax cuts were used to justify program cuts in the Obama administration.28 And the high deficits produced by the Trump tax cuts were used to justify program cuts during the Biden administration.29

If the Trump tax cuts, which disproportionately benefit the very well-off, are made permanent, their resulting deficits will be used to justify cutting programs that help educate, feed, house, and provide health insurance for a large portion of the U.S. population.

Switching to a current policy baseline for official budget enforcement violates budget law and effectively partially eliminates the filibuster

Opportunistically adopting a current policy baseline in 2025 as a rhetorical move to frame trillions of dollars of costs as being free is an expensive gimmick, but some congressional Republicans have talked about going a step further and adopting it for “budget enforcement”—how Congress adjudicates its official rules on what budget legislation is allowed to do.

Under official budget rules and the legal definition of a baseline written into budget law in 1990, switching to a current policy baseline for official budget enforcement in reconciliation is not allowed.30 The baseline and its rules are defined in statute, and the Senate parliamentarian has advised in the past against allowing statutory budget rules to be ignored in reconciliation. These rules do not prevent anyone from rhetorically claiming that extending tax cuts should be considered costless, and they do not prevent the CBO and the JCT from producing additional information that shows what the cost would be under a current policy baseline. But they do prevent its use in the official score, the score used to determine whether the Senate Finance Committee has met its reconciliation instruction and whether the bill produces deficits beyond 10 years.

Nevertheless, some Republicans, such as incoming Senate Finance Committee Chair Crapo, have suggested they would like to deviate from the official budget enforcement rules anyway.31 This would have to happen by abusing Section 312 of the Congressional Budget Act. A deeply abused Section 312 could allow the chairman of the Senate Budget Committee to simply assert that the official score is quite literally whatever he says it is, allowing him to fabricate a score from thin air.

Critically, the Senate parliamentarian has advised in the past that the budget chair does not have that authority. This would leave Republicans unable to use this maneuver unless the Senate parliamentarian is fired by incoming Senate Majority Leader John Thune (R-SD), ignored by the presiding officer of the Senate, or successfully encouraged to ignore precedent under threat of being fired.

This would, at a core level, be a large step toward eliminating the filibuster since it would allow the budget chair to go around most of the rules governing the special expedited process that allows budget legislation to be enacted with only a simple majority of votes in the Senate instead of 60.32 A chairman could ignore the Byrd rule limitation against long-term deficits by asserting they do not exist, as Sen. Crapo is musing. A chairman could ignore the Byrd rule limitation against being out of compliance with a committee’s reconciliation instruction, as Sen. Crapo is musing. Flagrant abuse of Section 312 of the Congressional Budget Act could go beyond what Sen. Crapo has mused. A chairman could ignore the prohibitions against modifying Social Security in reconciliation by asserting that Social Security is not modified. A chairman could determine nonbudgetary provisions are budgetary by simply asserting budgetary impacts. A reconciliation process that allows the chairman of the Senate Budget Committee to ignore most of its limitations approaches a regular order bill without the filibuster.

Brazen abuse of Section 312 of the Congressional Budget Act would render budget enforcement meaningless. It would allow the chairman, on a case-by-case basis, to fabricate points of order against bills or amendments that are, in fact, in order and pretend offending legislation is in order when it is not. It would allow the chairman to pretend all legislation they do not support violates the Congressional Budget Act’s rules while pretending all legislation they do support does not. Abusing Section 312 would make enforcement of the Congressional Budget Act fatuous. Using a current law baseline to make passage easier in 2017 while using a current policy baseline to make passage easier in 2025 would be such an abuse.

Conclusion

With large portions of the Trump tax cuts set to expire at the end of 2025, Congress has a significant decision to make, both for tax fairness and for the United States’ fiscal path. Any extension of the Trump tax cuts should be fully offset relative to a current law baseline. Congress should not repeat the mistakes it made when it extended large portions of the Bush tax cuts without paying for them. A bad extension of the Trump tax cuts is worse than not extending them at all.